Wake up call for charities – the Common Reporting Standard is here

Although the Common Reporting Standard (CRS) catches charities in its due diligence and reporting net, its potentially onerous impact remains largely unrecognised by the charities sector. As the first reporting year runs into its sixth month, we've been working with sector bodies and HMRC on assessing and (where possible) mitigating impact. Click here to read the latest update on your charity's potential obligations:

CRS is designed to combat international tax evasion by allowing countries to swap information on each other's tax payers. This is achieved by requiring banks and other 'Financial Institutions' to collect data on 'Account Holders' and report some of it to HMRC annually for onward global exchange.

Sounds worthy but dull? Guess again.

Those happily assuming that charities cannot be liable to collect and report alongside banks are in for a rude awakening. Many charities are caught by the counter-intuitive 'Financial Institution' definition and, as CRS came into force on 1 January this year, they should begin immediately to collect the required information on all beneficiaries of 2016 grants, regardless of grant size.

Below are our top ten key CRS points for the sector:

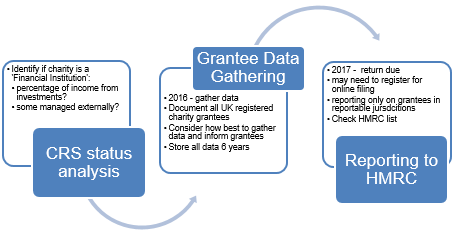

- Any charity may be affected – There is no charity exemption; a charity considered to be a 'Financial Institution' will have active obligations to HMRC, while others will merely have to self-certify their status as 'Active Non Financial Entities' to third parties such as banks.

- Those with managed investments are the most likely to be caught - Regardless of a charity's legal form, if more than 50% of incoming resources in the last three calendar years was derived from investments and at least some part of the charity's assets are managed by an external investment manager, the charity is likely to be caught as a 'Financial Institution' and required to gather data and report.

- Data collection is required NOW on all 2016 grantees – If a charity is caught as a 'Financial Institution', it must collect certain data on all individual and institutional grantees, wherever located and no matter the size of the grant, and retain this data for six years.

- Reporting in 2017 will be based on your 2016 grantee data –charities will have to file a return with HMRC by 31 May 2017 listing data in respect of grantees that are resident in certain jurisdictions that are participating in the CRS. It is expected that this can be filed online. For some charities not claiming Gift Aid, this may be the first contact with HMRC in years.

- Self-certification by grantees - The default CRS position is that grantees should be asked to self-certify their details, including their place of tax residency and tax ID number (if any). HMRC has indicated that this information may be collected verbally if necessary, as part of a grant application form or under a standalone form. A charity needs to have taken reasonable steps to collect the data, doing so ideally before the grant is made.

- UK grantees – Reporting charities will not have to include the details of grantees that are UK tax-resident on their CRS return (since the CRS is an international exchange arrangement) but they will have to establish formally that a grantee is UK resident. HMRC has helpfully accepted that reporting charities may assume that charities registered with the Charity Commission for England and Wales, Northern Ireland or the Office of the Scottish Charity Regulator registers are resident in the UK. HMRC has indicated that UK individuals who receive a grant can simply tick a box on the charity's grant application that they are UK resident.

- Participating Jurisdictions – The ever-expanding list of countries participating in CRS will change from time to time. When a reporting charity makes its Return to HMRC, it will report on those jurisdictions that are on HMRC's list for the reporting year. This means a charity's grantee may not be reportable in 2017 but may be in 2018.

- Gifts of goods alone are excluded – A reporting charity that hands out coats to Syrian refugees in Greece will not have to consider those gifts for CRS purposes while one that gives out cash for food and clothes will do.

- Data Protection – Reporting charities should ensure that they have explained to all grantees that their data may be reported to HMRC and, from there, exchanged abroad.

- Human rights – Some charities may be concerned that a grantee may be endangered if their information is ultimately provided back to their government. Grantees must be told of the possible information exchange. There is no exception for reporting in this scenario, but it is expected that a common sense approach to compliance on this point may be taken by HMRC, should charities feel that they have a reasonable excuse not to submit information on a particular grantee.

HMRC's general guidance manual on automatic exchange is now live and charities-specific guidance (on which HMRC will welcome comment) is expected shortly. HMRC is holding an informational event for charities on CRS on 29 June 2016. If you are interested in attending, please contact crs.consultation@hmrc.gsi.gov.uk.

For questions on CRS, do not hesitate to get in touch with Alana Petraske. This blog comes from Withers Worldwild, to see the original version please follow this link.